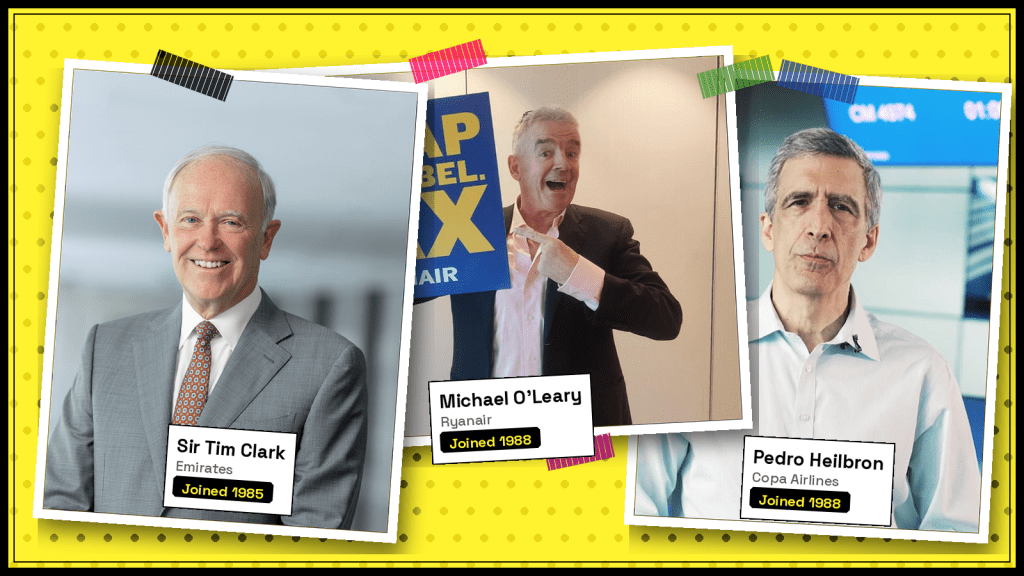

The Airline CEOs Who Don’t Leave

Michael O'Leary has tied himself to Ryanair until 2032. He belongs to a shrinking class of airline chiefs who have become almost impossible to replace – which is exactly what makes their eventual departures so risky.