U.S. Legacy Carriers Vs. Low-Cost Rivals in 8 Charts

Skift Take

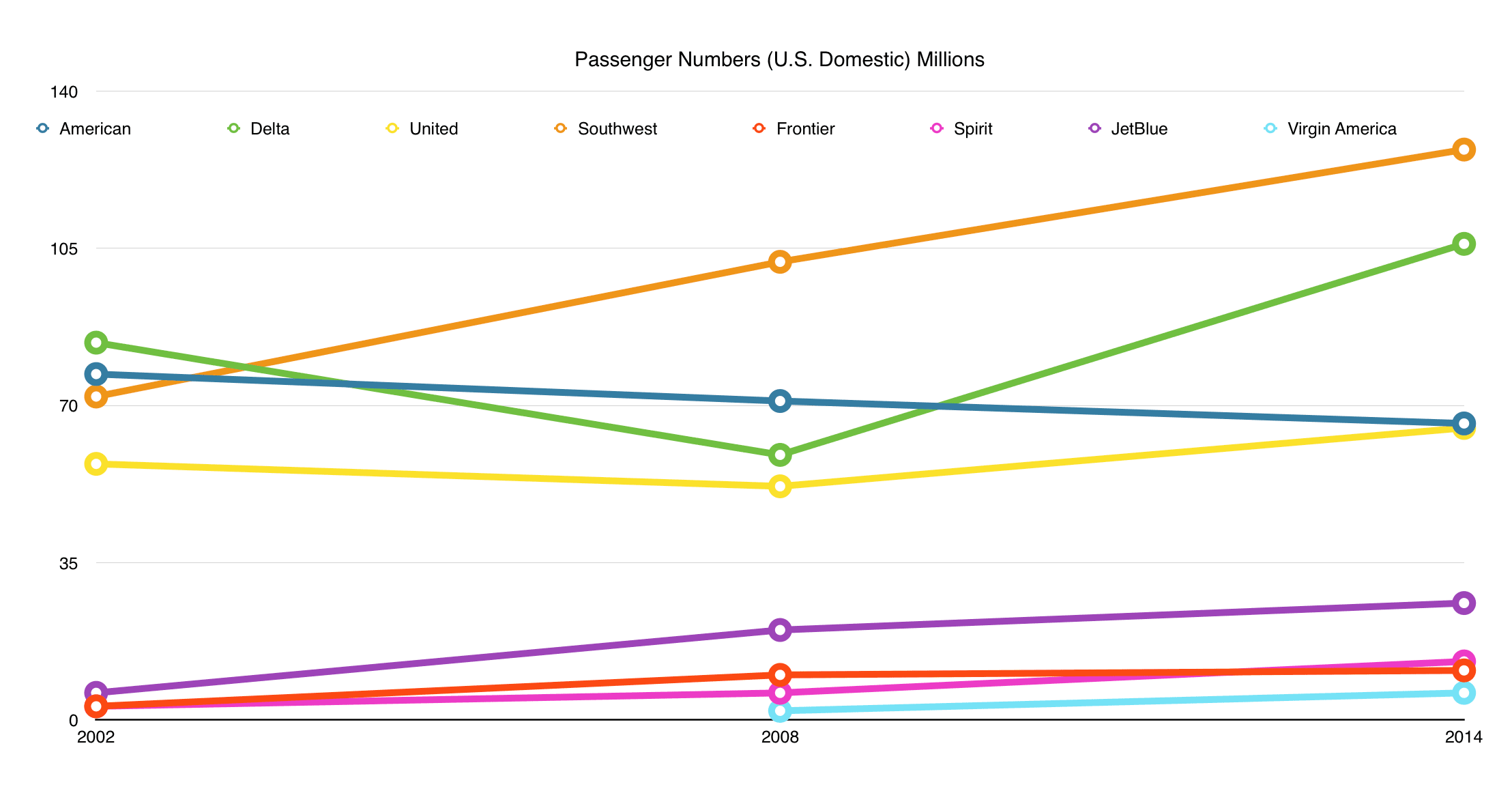

It's a big market, with plenty of passengers eager to fly around. In their own way, all airlines are making the most of this boom.

It is a truth universally acknowledged that a legacy airline in possession of a good market cannot handle competition.

To a degree, this notion has been validated by huge losses legacy airlines have incurred over the years, the industry’s notoriously poor margins, and market consolidation.

Some of these woes have been accredited to the rise of upstart low-cost carriers and ultra-low cost carriers taking market share away from those legacy carriers and pushing margins down through aggressive pricing.

More recently those full-service and bare bones carriers, have been joined in the market by a hybrid model, which we call low-cost lux. It is best characterized by boutique airlines which offer low-fares and up-scale service, such as JetBlue and Virgin America. Beyond different service models, these airlines have dramatically different operating models, which influence the market share they can expect to control, and the margins they can expect to make.

The perception i