Channel Shock: The Future of Travel Distribution

Photo Credit: Sabre Travel Network

Skift Take

The global distribution systems aren't going anywhere. Innovation, however, is happening in the margins of the travel distribution marketplace, with airlines seeking to regain control of their destiny.

[caption id="attachment_241353" align="alignright" width="300"] It’s our fifth birthday this week. Click on the logo for more big stories.[/caption]

The travel industry is always fixated on what’s new and sexy.

Whether it’s booking a hotel using Amazon Alexa, or checking your Priceline booking from your Apple Watch, we tend to focus on incremental improvements to how consumers book and experience their travel. Yet, the main system that sits underneath the snazzy interfaces, which actually connects hotels and airlines with online booking sites and travel agents, has its roots in a handful companies originally founded by U.S. and European airlines.

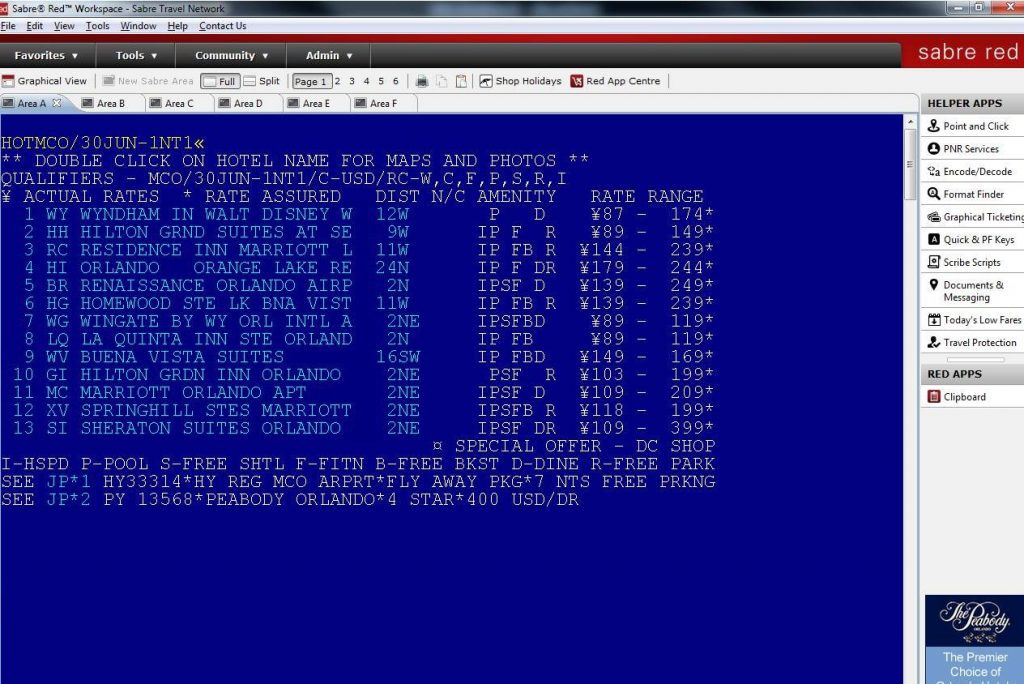

If you’re not deeply entrenched in the fields of travel distribution and technology, you may not know that the same type of technology has been used since the 1960s to handle transactions between travel providers like airlines and the companies that purchase travel for travelers.

After general aviation began to surge follow