Online Travel This Week

In online travel, selling flights tends to be a low-margin business, but charging travelers $20 to $40 to freeze airfares or room rates — and dealing with the consequent risk — now that’s where the real money is.

Frederic Lalonde, the founder and CEO of Hopper, the app best-known for its flights business, thinks eventually the entire travel industry will awake to what he estimates to be this $200 billion market opportunity in various fintech services.

Lalonde told Skift that around 70 percent of Hopper’s revenue these days comes from ancillary products, including price freezes, the ability to change flights for any reason up to 24 hours before departure, a rebooking service, and a price drop guarantee.

Forget about airline tickets: These ancillary/fintech products are even more profitable than Hopper’s hotel bookings, Lalonde said.

He said these fintech services — one can debate whether they are really fintech or ancillary add-ons — add around $40 to each Hopper transaction on average, and are way more profitable than the travel sale itself.

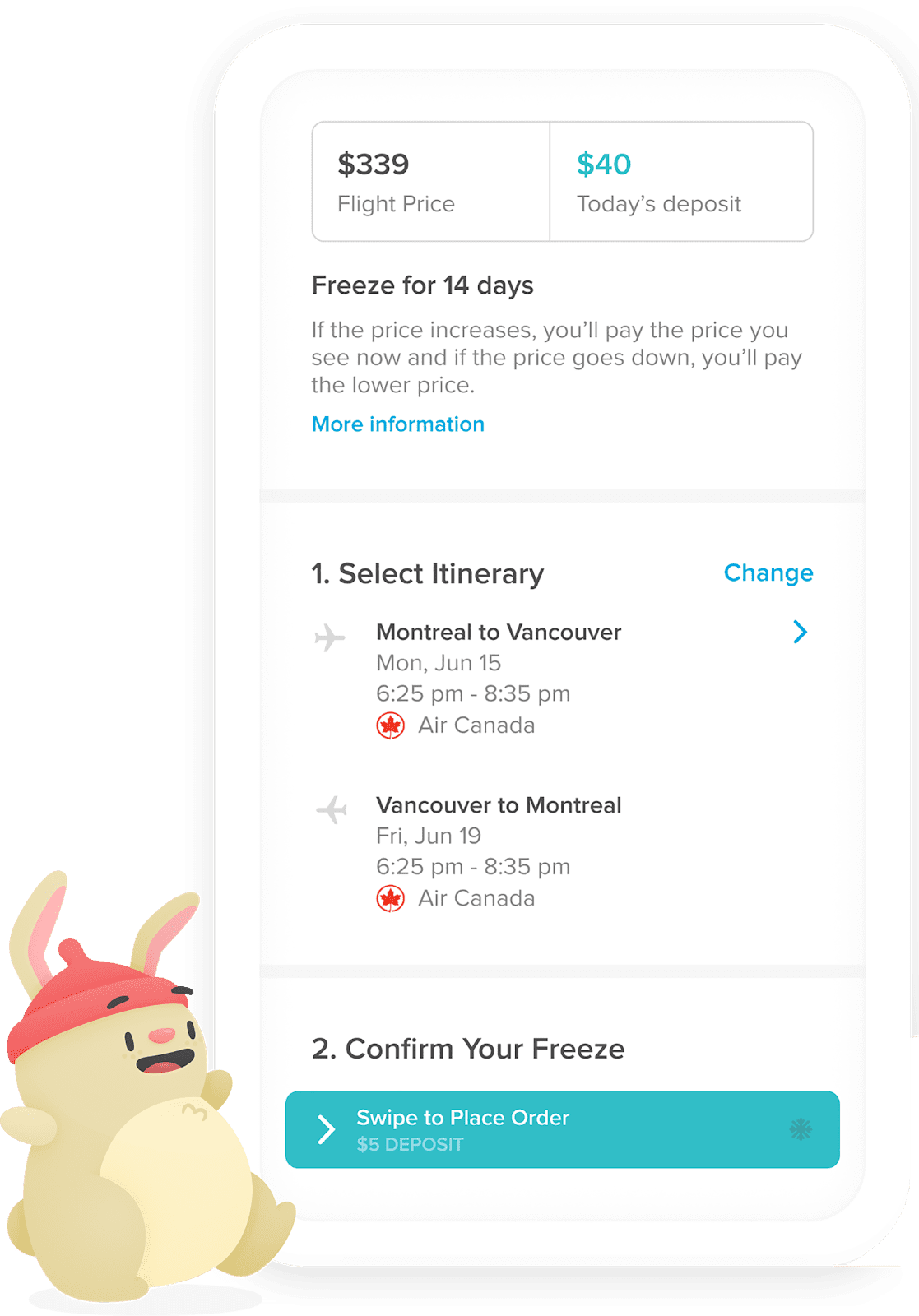

The way it works is a traveler can freeze an airfare at $400 for up to 15 days for a fee that might be $20 to $40, for example. The higher the risk that the airfare will rise the more Hopper would charge the flyer. But if the airfare rises $200, even though Hopper only collected perhaps $35 or $40 from the then Hopper pays the difference to the airline.

Lalonde argues that Hopper has a proverbial moat against competition because of its tech. Hmmm, let’s see : Moats tend to evaporate as competitors catch up.

“Basically everything is priced by machine learning and underpinned by the data we have,” Lalonde said.

If Hopper loses money on the transaction, it underwrites the risk, he said, which is “baked in and its on our P&L,” referring to Hopper’s profit and loss statement.

Hopper co-founder Joost Ouwerkerk (left) with founder and CEO Frederic Lalonde.

Hopper isn’t profitable: Lalonde said free cash flow is plowed back into marketing to spur growth, and there have been 60 million downloads of the Hopper app to date. He claimed, based on global distribution system-sourced MIDT (Marketing Information Data Tapes) that Hopper’s market share is 6 percent of all online travel agency flight bookings in the U.S.

That would be impressive.

We’ve been deservedly rough on Hopper over the years: The company raised $400 million since its launch in 2007, and took a startup eternity to launch a product, which doesn’t even resemble today’s Hopper, and to find its footing.

But it appears to have done so. Hopper, which is privately held, claims to have seen 100 percent year over year revenue growth in Covid-ravaged 2000. How? Lalonde claims the company was up 600 percent in revenue in the first few months of that year because of the fintech products it debuted a couple of years earlier, and it doubled its market share in hotels. Alternative accommodations are on the way, too.

Over the last few years, Hopper has been busy executing acqui-hires: Journy in June — you read it here first — as well as OptionsAway, Gravy.AI, and GDX Travel, all in 2019.

Hopper is not profitable — and personally I really don’t care. Financial engineering can make many companies profitable. But Hopper is focused on growth and taking market share.

Lalonde said there has never been more private capital available, demand has never been higher, and consumers have a ton of savings. “We think there will be two years of that,” he said.

The company launched Hopper Cloud in the business-to-business realm, and it is poised to power travel for investor CapitalOne, with little spend required to acquire customers because of CapitalOne’s customer base.

I don’t know how long Hopper’s competitive moat will last, but it appears to have a decent head start.

In Brief

Kayak Officially Debuts Its Business Travel Product

This is not indeed the most elongated launch in travel history, but Skift’s Matthew Parsons credibly calls out Kayak for falling short on the foundation of its corporate travel play, Kayak for Business, namely a lack of customer service. Hey, few road warriors are traveling right now, but when they do, they will want customer service humans to fix stuff. Skift

Tripadvisor Plus Unleashes a Hotel Tie-In for Channel Managers

Global distribution system bypass? Yes, a minor one of sorts. Tripadvisor’s new subscription service, Tripadvisor Plus, now lets independent hotels connect to the program through their channel managers and booking engines in a way that dodges pricy booking fees from Sabre and Amadeus. Skift

Homegrown Russian Online Travel Agencies Play to Their Strengths

Native Russian online travel agencies know they can’t compete with competitors such as Booking Holdings in paid search, but they can tap into alternative business models, and seize on the citizenry’s tendency to shop for travel patriotically. Skift

Subscribe to Skift Pro to get unlimited access to stories like these

{{monthly_count}} of {{monthly_limit}} Free Stories Read

Subscribe NowAlready a member? Sign in here

Subscribe to Skift Pro to get unlimited access to stories like these

Your story count resets on {{monthly_reset}}

Already a member? Sign in here

Subscribe to Skift Pro to get unlimited access to stories like these

Already a member? Sign in here