In our latest report, Skift Research analyzes the often overlooked market for multi-day tours and activities.

The classic tour operator is a manufacturer of sorts. These tour operators build a new travel product by piecing together many different parts from across the travel sector. A hotel here, a flight there, and a restaurant or two to bring it all together. With all of these different travel components to build with, it’s no surprise that tours are a complex area.

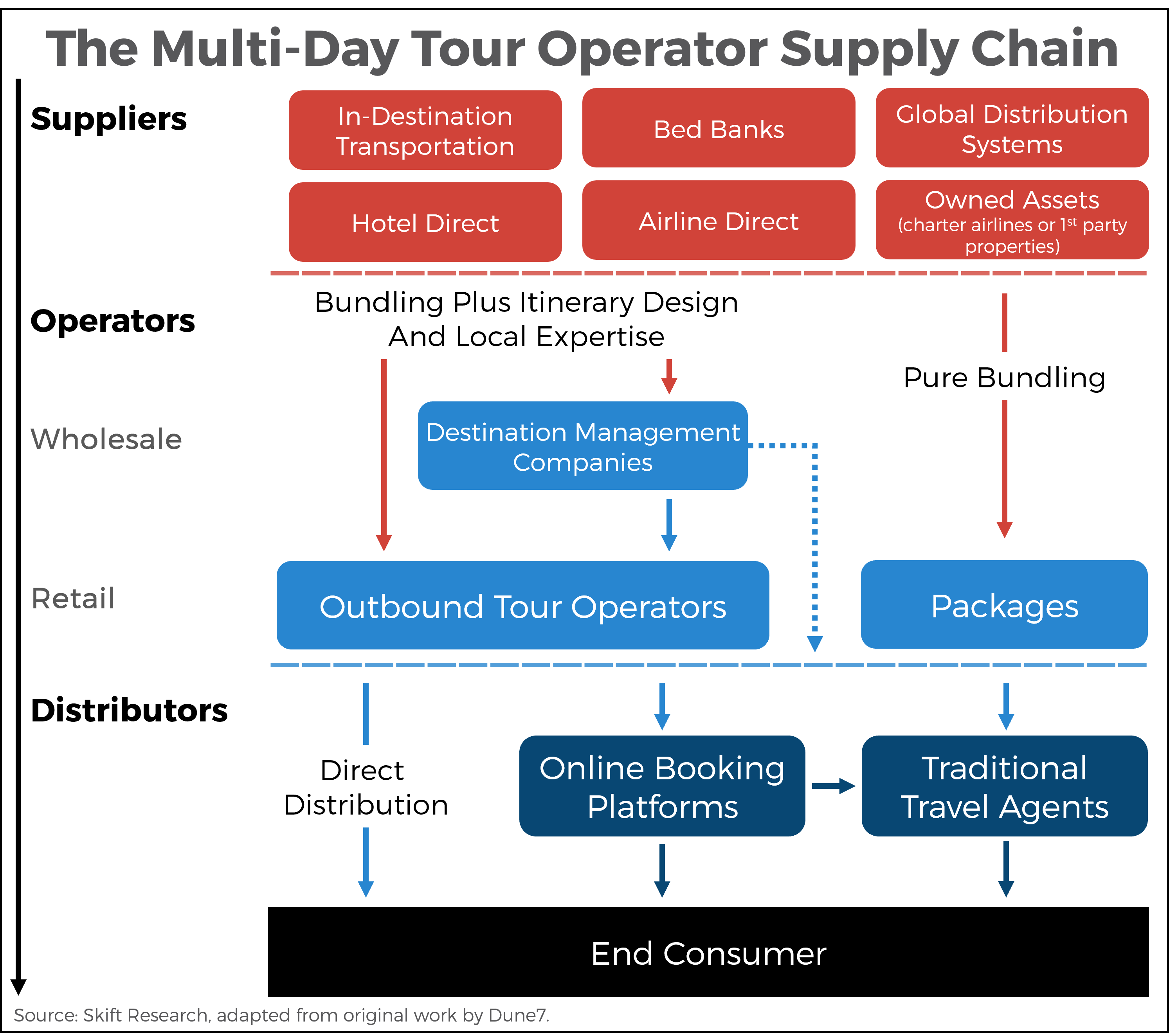

The below excerpt focuses on understanding the tour operator supply chain and making some sense of how many different types of tour businesses relate to and interact with one another.

The full report dives deeper into the sector, exploring how the sector’s supply chains and distribution networks are responding to changes in technology. It also looks at the changes brought about by COVID-19 and how tours have responded.

Preview and Buy the Full Report

The Tour Operator Supply Chain

Let’s examine the lifecycle of how a tour is created and comes to market in the land-based tour operator space.

Our model of the tour operator chain has three layers of value add. It starts with the supply of core travel products like hotels, flights, trains, and cars. These ‘raw materials’ of the tour might come from direct contracting with an airline or via a reseller like a bed bank. Some fully integrated tour operators even own their own charter airline or resort properties.

The next layer is the tour operator itself. “The tour operator is the manufacturer,” says Catherine Prather, President of the National Tour Association. Unlike a hotel or airline that is fundamentally anchored to a physical asset, tour operators sell a value-added travel service not tied to a single tangible product. By that we mean that tour companies ‘assemble’ unique trips by taking building blocks from other travel suppliers and adding an additional layer of intangible value-add. That value-add might be local expertise, cheap bundled pricing, or peace of mind. This transforms the raw materials into a more valuable new product which they can resell into the marketplace.

We distinguish here between tour packagers that are doing pure bundling and itinerary-based tours where an additional layer of in-destination curation and expertise is used in the ‘manufacturing’ process. A company like TUI is still a multi-day tour operator at this tier. It ‘manufactures’ its own tour products and retails them through first-party channels and also re-sells through agents and other distribution channels. But the tour products it offers are mainly a bundling of different supply components. In contrast, a G Adventures both bundles the supply components and adds an additional design component by planning daily activities and arranging for local guides.

There is also the opportunity in this layer for wholesalers and retailers. Specialist DMCs often design local tours that can be resold to larger retail travel agencies that can tap into their local market of outbound travelers.

The final layer is that of distribution. There are three primary channels. First is the direct channel driven by in-house sales and marketing efforts. Then there are the two major intermediaries in the space, online booking sites, which operate on both commission and advertising models, and travel agents. It should be noted that tours are one of the last great bastions of traditional travel agents (along with business travel). A very significant volume of tour products is distributed by the large travel consortia and even, in some countries, by brick-and-mortar retailers. This is because tours are one of the most complex travel products, a result of the above ‘manufacturing’ process, making a human intermediary much more valuable.

A hotel room might have a handful of core attributes (star rating, price, location, room type) and several more secondary ones (Wi-Fi, pool, view, floor height). But even the most basic tour can have dozens or more key attributes (departure date, size of group, length of trip, itinerary variations, level of physical activity, type of accommodation, age of participants, etc.). This creates difficulty to code for tours in the back end, as well as for consumers to shop and compare multi-day tours. This has made it doubly hard for online booking sites to take off in the space; however, these challenges are slowly but surely being overcome and digital platforms are growing in prominence as distributors of tours.

We understand that we have tried to simplify a very complex space and so there may be many nits to pick with this diagram. But we think that these core mental models of three main tour products (packages, itineraries, and cruises) sold via layers of value (supply, operation, and distribution) is a useful way to help decipher the tangle of different operators in this industry.

A lot of the confusion in the space seems to stem from the many different permutations of how vertically integrated an organization chooses to be and what permutation of products they choose to sell. But by building this mental model of the industry we can better see past the superficial differences of each specific company. A lot of the variation we see across tour companies is often reflective of different choices about what parts of the value chain to vertically integrate and what products to sell. But within each specific part of the value chain in isolation, business models are often more similar than they may first appear.

For example, tour operators that run their own in-destination programs vs. ones that outsource to a DMC are not two fundamentally different types of tour companies but are instead making different decisions about how vertically integrated they want their organizations to be. Or a travel agent that sells tour packages is best thought of as vertical integration between the ‘manufacturing’ stage of packaging process and a distribution channel, rather than as a wholly separate kind of company from a tour operator with a large first-party salesforce.

Preview and Buy the Full Report

Subscribe now to Skift Research Reports

This is the latest in a series of research reports, analyst sessions, and data sheets aimed at analyzing the fault lines of disruption in travel. These reports are intended for the busy travel industry decision-maker. Tap into the opinions and insights of our seasoned network of staffers and contributors. Over 200 hours of desk research, data collection, and/or analysis goes into each report.

After you subscribe, you will gain access to our entire vault of reports, analyst sessions, and data sheets conducted on topics ranging from technology to marketing strategy to deep dives on key travel brands. Reports are available online in a responsive design format, or you can also buy each report à la carte at a higher price.

Subscribe to Skift Pro to get unlimited access to stories like these

{{monthly_count}} of {{monthly_limit}} Free Stories Read

Subscribe NowAlready a member? Sign in here

Subscribe to Skift Pro to get unlimited access to stories like these

Your story count resets on {{monthly_reset}}

Already a member? Sign in here

Subscribe to Skift Pro to get unlimited access to stories like these

Already a member? Sign in here